2025 Tax Updates

As we move into a new year, tax season has a way of sneaking up on all of us. With April just around the corner, now is the time to shift from reactive to proactive — especially given the number of tax law changes that are taking effect for the 2025 tax year. Our goal with this update is to help you understand what’s changing, what may apply to you, and how to approach your filing with clarity and confidence, so you can stay focused on what matters most in your life.

Last year’s passage of the One Big Beautiful Bill Act (OBBB) marked the most significant shift in tax policy since the Tax Cuts and Jobs Act of 2017. Many provisions that were once temporary are now permanent, and several new rules are officially in effect for 2025. As a result, filing this year may feel a bit more complex than usual. Below, we’ve outlined the most important updates — including changes to tax brackets, deductions, credits, and new planning opportunities — to help you know what to look for as you prepare your return.

As always, we believe the best outcomes come from a collaborative approach. We regularly work alongside a trusted Network of Professional Strategic Partners — including CPAs and other financial professionals — and are happy to coordinate with the advisors you already use. By sharing insights and staying aligned, we aim to ensure your financial, tax, and planning strategies are comprehensive, streamlined, and working together in your best interest. As you review the updates below, circle anything that raises questions and bring it to your tax professional — and know that our team is here to support the process every step of the way.

Important Updates

for the 2025 Tax Year

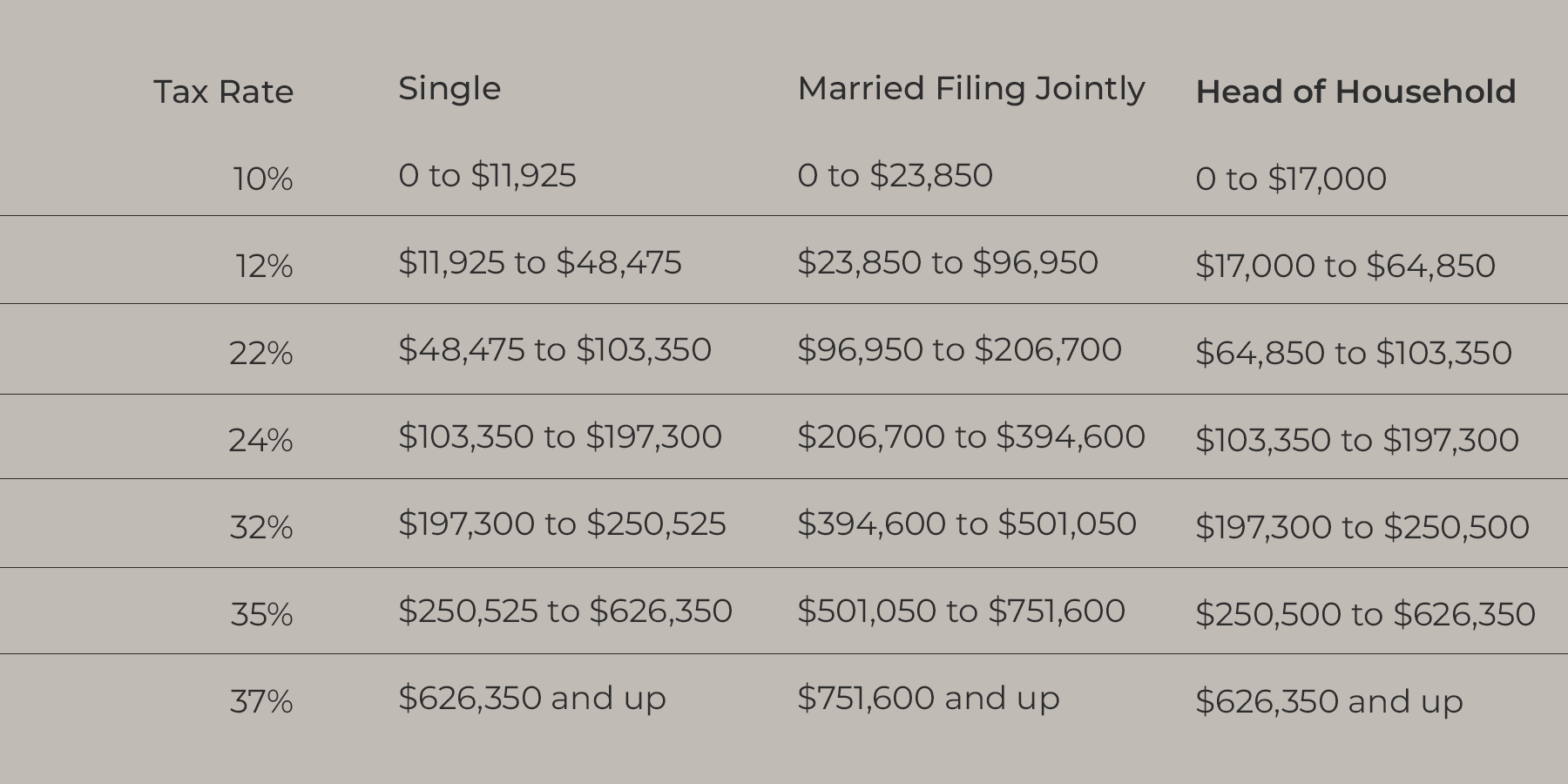

CHANGES TO FEDERAL TAX BRACKETS1

As it often does, the IRS has adjusted the 2025 tax brackets based on inflation. The brackets for the 2025 tax year are as follows:

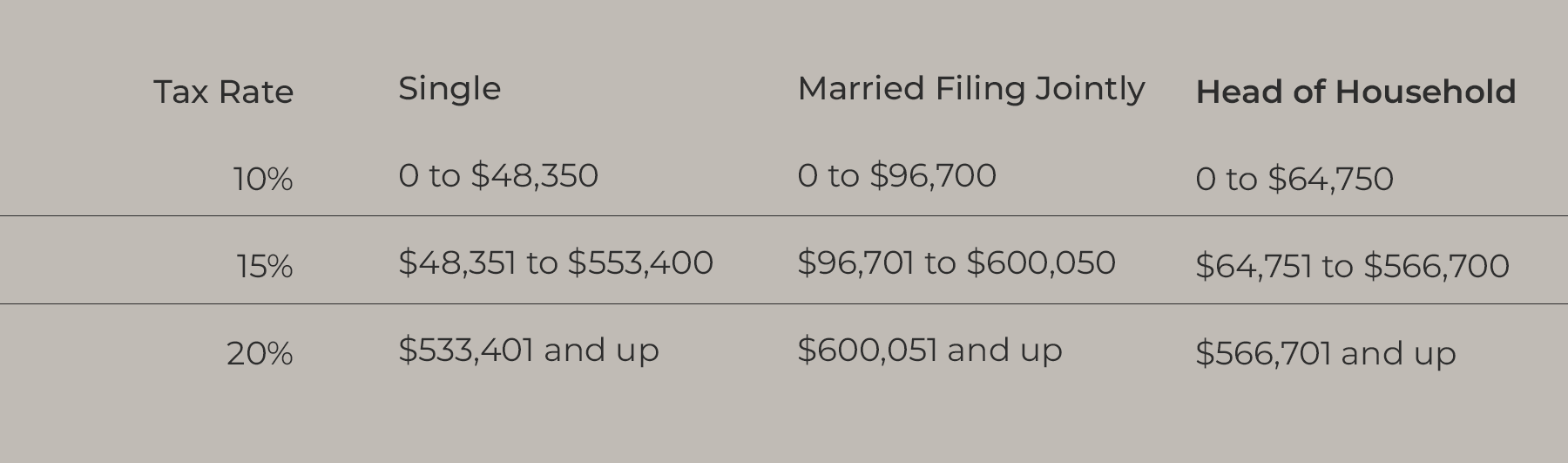

CHANGES TO CAPITAL GAINS2

The income threshold for long-term capital gains rates has also gone up.

According to the IRS, there are also a few exceptions where capital gains may be taxed at a higher rate. Those exceptions include when selling certain types of small business stock (taxed at a maximum 28% rate), selling collectibles such as coins or art (also a maximum 28% rate), and selling certain types of depreciable property (maximum 25% rate).

CHANGES TO DEDUCTIONS

Several tax deductions have increased due to the OBBB. For example, the standard deduction has been raised from $15,000 to $15,750 for single individuals, and from $30,000 to $31,500 for married couples filing jointly. For Heads of Household, the standard deduction is now $23,625, up from $22,500.3

For those who choose to itemize their tax deductions, the OBBB also increases the state and local tax (SALT) deduction limit from $10,000 to $40,000. This deduction will increase by 1% each year until 2030, when the cap reverts back to $10,000. Note that the SALT deduction begins to phase out for taxpayers earning $500,000 or more in annual income.4

There is also a new temporary personal deduction available specifically to seniors. Anyone born before January 2, 1961, may claim a $6,000 deduction if their annual income is $75,000 or less. (Married couples filing jointly may claim up to $12,000 so long as their combined income is $150,000 or less.) This deduction phases out above these limits, ending at $175,000 for individuals and $250,000 for couples.5 Note that this new deduction isn’t permanent and will expire after 2028.

Finally, the exemption on estate and gift taxes is now $15 million (up from $13.99 million).6

CHANGES TO TAX CREDITS

The OBBB also enacted some important changes to several types of tax credits — raising one while essentially eliminating others.

First up is the child tax credit, which has now been permanently increased to $2,200, up from $2000 previously. This credit applies to all children who were under 17 by the end of 2025. Note, however, that parents with an annual income of more than $200,000 ($400,000 if married and filing jointly) can only claim a partial credit, not a full one.7

Certain “green” or “clean” tax credits have now expired, however. That includes credits for buying new and used electric vehicles or installing energy efficient heating and cooling systems, including rooftop solar panels. So, if you bought a new electric vehicle after September, you won’t be able to claim a credit for it. (However, you may be able to claim a credit if you purchased solar panels or a more energy-efficient HVAC system through December of 2025, so it’s still worth looking to see whether this credit applies to you.)

NEW RULES FOR 401(k) CATCH-UP CONTRIBUTIONS FOR HIGH EARNERS 8

One important retirement planning change that is getting less attention — but could have a meaningful impact — involves 401(k) catch-up contributions for high-income earners.

Beginning in 2026, individuals who earned more than $145,000 (indexed for inflation) in the prior year and are age 50 or older will be required to make their catch-up contributions to a Roth account, rather than on a pre-tax basis. This means those additional contributions will be made with after-tax dollars.

Why does this matter?

For years, many high earners used catch-up contributions as a way to further reduce taxable income in peak earning years. Under the new rule, while you can still contribute, the tax treatment changes. Contributions will no longer lower your current taxable income — but qualified withdrawals in retirement will be tax-free.

There are a few important planning considerations here:

If your employer does not offer a Roth 401(k) option, the catch-up requirement may be delayed until they do.

This shift may accelerate conversations around Roth conversion strategies.

It reinforces the importance of tax diversification — having assets in pre-tax, Roth, and taxable “buckets” to provide flexibility in retirement.

For those in their highest earning years, it may change how aggressively you choose to defer income versus building after-tax assets.

For many high-income professionals, this isn’t a negative change — it’s simply a different lever to plan around. But it does mean retirement contribution strategies deserve a fresh look as part of your broader tax and cash-flow planning.

As always, the key is coordination. Retirement plan design, compensation structure, and tax strategy should work together — not in silos.

If you have questions about how these new rules apply to you, we’re happy to review your current contribution elections and help you think through the tradeoffs before year-end.

CHILD SAVINGS ACCOUNTS 8

The OBBB introduced an interesting provision: A new type of tax-advantaged savings account specifically for children born in 2025 through 2028. So, if you or a loved one welcomed a new baby in 2025 you can file Form 4547 along with your tax return. In response, the government will make a one-time deposit of $1,000 into a tax-deferred investment account. Parents and relatives can contribute up to $5,000 a year, and employers can also kick in $2,500. (Note that employer contributions count toward the $5,000 limit.) Any earnings are tax-deferred until the child reaches 18, however withdrawals after that point will be taxed as ordinary income.

These accounts can be a handy way to help children save for the future, including higher education. However, there are many rules regarding these accounts, and they may not always be the best option compared to alternatives. For these reasons, let’s chat before you or your family decide to open one!

TAXES ON OVERTIME PAY

Finally, you may have heard that, thanks to the OBBB, there are now no taxes on overtime pay. Unfortunately, this is not quite accurate. In reality, certain workers can claim a deduction on a portion of their overtime pay. The maximum deduction is $12,500 for individuals and $25,000 for joint filers. Note that the full deduction is available only for those with an annual income of $150,000 or less ($300,000 for those filing jointly.) The amount phases out above this level and is not available for individuals with an income over $275,000 and couples over $550,000.5

Sources

1 “2025 Tax Brackets,” Tax Foundation, https://taxfoundation.org/data/all/federal/2025-tax-brackets/

2 “Capital gains and losses,” Internal Revenue Service, https://www.irs.gov/taxtopics/tc409

3 “Notable changes under the One, Big, Beautiful Bill,” Internal Revenue Service, https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill |

4 “SALT deduction,” Reuters, https://tax.thomsonreuters.com/en/glossary/salt-deduction

5 “One, Big, Beautiful Bill Act: Tax deductions for working Americans and seniors,” Internal Revenue Service, https://www.irs.gov/newsroom/one-big-beautiful-bill-act-tax-deductions-forworking-americans-and-seniors

6 “One, Big, Beautiful Bill provisions,” Internal Revenue Service, https://www.irs.gov/newsroom/one-bigbeautiful-bill-provisions

7 “Child Tax Credit,” Internal Revenue Service, https://www.irs.gov/credits-deductions/individuals/child-tax-credit

8 “Understanding new Roth 401k catch up rules,” Fidelity, https://www.fidelity.com/learning-center/personal-finance/401k-catch-up-contributions-high-earners?ccmedia=LinkedIn&ccchannel=social_organic&cccampaign=Fidelity_Viewpoints&ccdate=202602&cccreative=Feb_17_401(k)_Catch_Up&ccformat=newsletter

9 “How Trump accounts for kids will work,” CBS News, https://www.cbsnews.com/news/trump-accounts-kids-explained/

Disclosure: Hilltop Wealth Advisors, LLC is an SEC registered investment adviser. Registration does not infer a certain level of experience or knowledge. This platform is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Hilltop Wealth Advisors, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Hilltop Wealth Advisors, LLC unless a client service agreement is in place.

As a registered investment advisory firm, we are restricted from posting, publishing or otherwise disclosing any form of testimonial which is related to our investment advisory services. LinkedIn recommendations and endorsements may be viewed as a testimonial. This policy requires that we block any recommendations or endorsements.

Links to websites and other resources operated by third parties are provided as information only, and there can be no assurance as to its accuracy, suitability or completeness. Hilltop Wealth Advisors, LLC does not endorse, authorize or sponsor the content or its respective sponsors and is in no way responsible for third party content, services, products or information, or for the collection or use of information regarding the web site’s users and/or members.

“Likes” are not intended to be endorsements of our firm, our advisors or our services. Please be aware that while we monitor comments and “likes” left on this page, we do not endorse or necessarily share the same opinions expressed by site users. While we appreciate your comments and feedback please be aware that any form of testimony from current or past clients about their experience with our firm is strictly forbidden under current securities laws. Please honor our request to limit your posts to industry-related educational information and comments.