Your DUKE University Legacy

MAXIMIZED

Hilltop Wealth Advisors specializes in helping employees of Duke University—and other institutions and companies in the Triangle—capitalize on their benefits to maximize their income.

We’re here to help you better understand the benefits you may be receiving from Duke University and leverage financial opportunities to build your portfolio, make strategic investments, save, and reduce taxes.

Learn more through a complimentary consultation with a Hilltop Advisor.

DUKE University BENEFITS +

Opportunities

Learn about your possible company benefits and

discover financial opportunities that could await you.

-

If you are enrolled in a Duke Advantage Plan (a High Deductible Plan), then you have access to a Health Savings Account. Duke may contribute to this account and you can make additional, tax-deductible contributions up to the annual limit. The earnings in this account are tax-deferred, and the withdrawals are tax-free if you use the funds for qualified medical expenses.

OPPORTUNITIES:

With an HSA, you do not have to deplete the account by the end of the calendar year. Instead, you could focus on building up the balance and investing it to take advantage of long-term market performance, and use the funds for future medical expenses. You can also take an HSA distribution at any point to reimburse yourself for previous medical expenses, if those expenses were incurred after the HSA was first opened.

-

This retirement plan is a traditional defined benefit pension plan that is available to employees at Duke University who are paid bi-weekly. It is funded entirely by Duke, and your future benefit is calculated based on your page, pay, and years of service. At retirement this plan provides monthly income and is calculated based on your age, pay, and years of service.

OPPORTUNITIES:

Be sure to run Duke’s pension estimator to see what your benefit might be at retirement, including your payout options ranging from Single Life to Joint and Survivor. These are irrevocable decisions so make sure to fully evaluate both retirement and pre-mature death scenarios for each payout option. Choosing the single life option may mean a higher payout now but much less for your spouse in the future.

-

If your income exceeds 150% of the Social Security taxable wage base, you may be eligible to contribute to Duke’s 457b Plan. This is an additional retirement plan that allows you to make pre-tax contributions up to the annual contribution maximum.

OPPORTUNITIES:

This plan provides an additional opportunity to save pre-tax beyond contributions to your 403b making it an excellent option for high income earners looking to further reduce their taxable income. In addition, there is no early withdrawal penalty for the 457b. Those planning to retire before age 59 and a half, or just wanting more flexibility, could benefit most from utilizing this plan. In addition to a wide range of investment options the 457b offers the ability to utilize a professionally managed strategy through an approved Fidelity advisor, such as Hilltop Wealth Advisors. Fully incorporating each of your retirement accounts into your overall investment strategy ensures all assets are working together as you plan towards your retirement.

-

This grant pays up to 75% of Duke’s weighted-average undergraduate tuition (tuition only) after a per-term deductible. Eligible full-time University employees need five consecutive years of service. Children, through age 26, seeking a first bachelor’s at accredited school qualify. The grant is limited to 16 semesters per employee and eight per child. Tuition-designated aid reduces the grant and these benefits may be taxable if the child isn’t a dependent.

OPPORTUNITIES:

Make sure to have funds set aside for tuition even if you qualify for this benefit. In-state UNC system tuition is often below the CTG deductible and typically only able to offset tuitions at private or out-of-state schools. Make sure to offset 529 plan withdrawal from the CTG benefit to avoid taxable 529 plan earnings.

-

The Faculty & Staff 403b Retirement Plan is available to Duke University employees who are paid monthly or bi-weekly. It has a variety of investment options and allows you to make two different types of contributions: pre-tax and Roth. With these contributions, you are subject to the annual salary deferral limit. If you are paid monthly, Duke will contribute 8.9% - 13.2% of your income to the 403b.

OPPORTUNITIES:

This plan offers a wide range of investment options, as well as the ability to utilize a professionally managed strategy through an approved Fidelity advisor, such as Hilltop Wealth Advisors. Fully incorporating each of your retirement accounts into your overall investment strategy ensures all assets are working together as you plan towards retirement.

Hilltop

Executive

Advantage

Hilltop Wealth Advisors specializes in retirement and wealth strategies designed for Duke Universtiy employees like you.

See how we can help you leverage your company benefits to maximize your financial legacy.

-

Risk-managed portfolio design—inside and outside of your retirement plan—helping you to work towards your wealth goals.

-

Comprehensive tax projections. Social Security timing and charitable giving strategies to chart a future worth planning for.

-

Guidance on HSA investing, Medicare integration, and retiree medical plan coverage with the Cisco Retiree Medical Access Plan.

-

Strategies for efficient distributions, Roth conversions, and tax-smart withdrawal sequencing.

-

Strategies for efficient distributions, Roth conversions, and tax-smart withdrawal sequencing.

-

Beneficiary reviews, trust coordination, and multi-generational planning in coordination with your estate attorney.

-

Experienced guidance on managing concentrated Cisco equity positions and equity compensation (restricted stock and employee purchase plans).

-

Leverage charitable giving tools to maximize your impact.

-

Planning for dependents, special needs and succession—so your wealth serves your family for generations to come.

Get STARTED.

Use the calendar to book a complimentary consultation with a Hilltop Wealth Advisor or give us a call.

Phone

919-401-1500

HOURS

M-F, 8AM-5pm (ET)

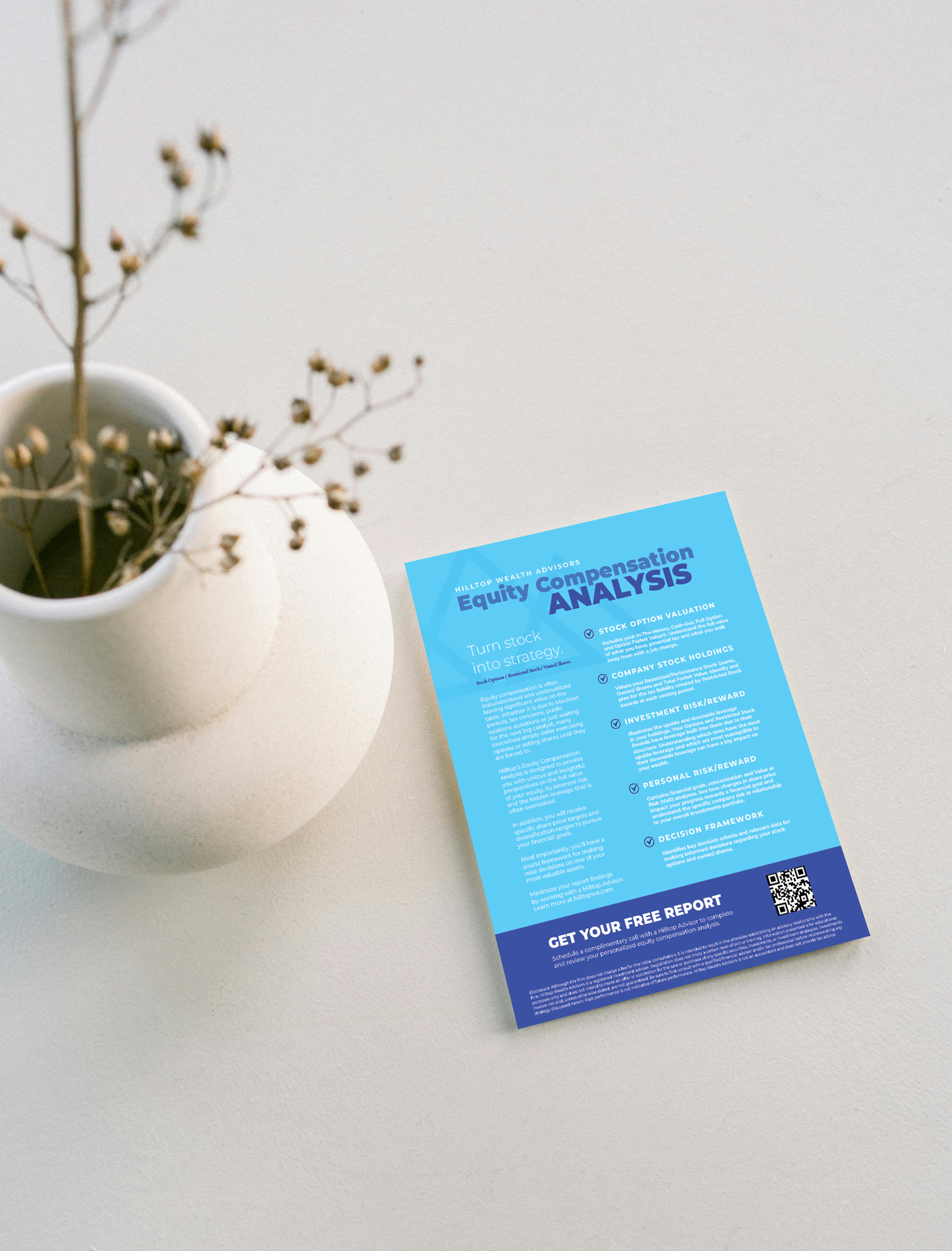

Have equity compensation?

Make wise decisions about one of your most valuable assets with Hilltop’s Equity Compensation Analysis. Designed to provide you with unique and insightful perspectives on the full value of your equity, its inherent risk, and the hidden leverage often overlooked in your stock options to help you reach your financial goals.

Disclosure: Hilltop Wealth Advisors is a registered investment adviser. Registration does not imply a certain level of skill or training. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance. Hilltop Wealth Advisors is not an accountant or attorney and does not provide tax or legal advice. Hilltop Wealth Advisors and Duke University are under separate ownership. Although the firm does not charge a fee for the initial complimentary consultation, it is intended to result in the attendee establishing an advisory relationship with the firm. Hilltop Wealth Advisors is not endorsed by Duke University or its affiliates.